Transrail Bags ₹2,752 Cr Orders

- 28th February 2025

Aaj Ka Bazaar

The sell-off on Wall Street also came as President Donald Trump clarified that previously paused 25% tariffs on imports from Mexico and Canada will go into effect on March 4. Asian equities fell Friday after heavy selling on Wall Street as traders grappled with underwhelming Nvidia Corp. results, further details on US tariffs and mixed economic data. Indian market may also drift lower on Friday after US President Donald Trump said his proposed 25% tariffs on Mexican and Canadian goods would take effect on March 4, along with an extra 10% duty on Chinese imports over the fentanyl opioid crisis. India’s Q3 GDP data is due later in the day, and it is estimated that weak urban consumption, along with moderation in real estate activity, will likely drag economic growth. On stock-specific news, A Singrauli Punarasthapan charge of Rs 300 per tonne, over and above the notified price of coal, will be levied uniformly across all mines of Northern Coalfields (Coal India subsidiary) effective May 1. The expected additional revenue will be around Rs 3,877.50 crores.

Markets Around Us

BSE Sensex – 74,607.56 (0.01%)

Nifty 50 – 22,324.95 (-0.98%)

Bank Nifty – 48,308.95 (-0.89%)

Dow Jones – 43,178.43 (-0.14%)

Nasdaq – 18,550.63 (-2.75%)

FTSE – 8,756.21 (0.28%)

Nikkei 225 – 36,999.65 (-3.28%)

Hang Seng – 23,139.65 (-2.40%)

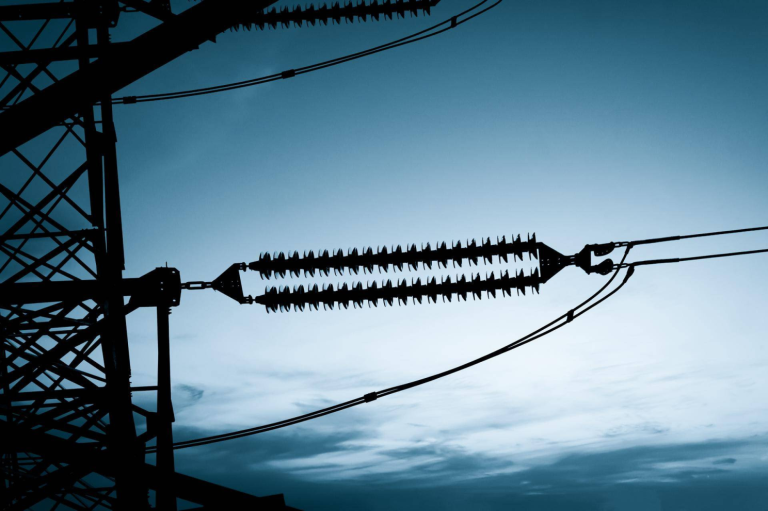

Sector: Heavy Electrical Equipment

Transrail Secures ₹2,752 Cr Orders, Shares Surge

Transrail Lighting’s stock surged over 6% in early trade on Friday after securing ₹2,752 crore worth of new orders in the Transmission & Distribution (T&D) segment, pushing its total order book beyond ₹7,400 crore. This marks a nearly 90% growth in order inflows compared to last year. The company, a key player in EPC projects across T&D, Civil, Railways, and Lighting, has a strong execution track record with over 200 completed projects in 58 countries. Despite this boost, Transrail’s stock has declined 3% in the past month and over 11% year-to-date. The stock had a strong IPO debut in December 2024, listing with a 36% gain, but has since dropped over 11% from its peak of ₹719.15 in January. With a growing order pipeline, solid manufacturing capacity, and execution strength, the company expects positive growth in the coming quarters, making it one to watch for traders and investors.

Why it Matters:

Transrail Lighting’s ₹2,752 crore order win significantly strengthens its order book to ₹7,400 crore, reflecting a strong growth trajectory in the Transmission & Distribution sector. This highlights the company’s increasing competitiveness and ability to secure large projects, reinforcing confidence in its long-term potential.

NIFTY 50 GAINERS

COALINDIA– 372.45 (2.36%)

SHRIRAMFIN – 618.00 (1.85%)

GRASIM – 2347.95 (0.34%)

NIFTY 50 LOSERS

INDUSINDBK – 990.30 (-5.39%)

M&M – 2631.10 (-3.50%)

TECHM – 1533.05 (-3.48%)

Sector: Pharma

Mankind Pharma's Merger Approved by NCLT

Mankind Pharma has received approval from the National Company Law Tribunal (NCLT) for the merger of Shree Jee Laboratory, JPR Labs, and Jaspack Industries, with the official merger date set as April 1, 2024. Once the order is filed with the Registrar of Companies, the three companies will be dissolved and integrated into Mankind Pharma. The company, known for pharmaceutical formulations and consumer healthcare brands like Manforce, Prega News, and Unwanted 72, continues to hold strong market positioning. Mankind Pharma’s stock had a strong debut in May 2023, listing at ₹1,422 per share—a 31.7% premium over its issue price. It later peaked at ₹3,054 in December but has since declined by 25% to ₹2,294 due to a broader market sell-off. Despite recent weakness, the merger is expected to strengthen the company’s operations, potentially improving long-term growth prospects.

Why it Matters:

Mankind Pharma’s merger with Shree Jee Laboratory, JPR Labs, and Jaspack Industries strengthens its business by integrating key subsidiaries, enhancing operational efficiency. The stock, which once peaked at ₹3,054, has dropped 25% due to market sell-offs, making it a crucial watch for investors. This consolidation could drive long-term growth, reinforcing Mankind Pharma’s leadership in pharmaceuticals and consumer healthcare.

Around the World

Asian stocks fell sharply on Friday, led by declines in Japan and South Korea, as local tech shares followed a major sell-off in Nvidia on Wall Street. Despite strong earnings, Nvidia’s stock dropped due to concerns over profit margins, impacting global tech stocks. Japan’s Nikkei 225 lost 3.2%, with SoftBank and Tokyo Electron falling over 5%, while South Korea’s KOSPI declined 3.1% as Samsung and SK Hynix tumbled. Indian and Australian markets also opened lower. Meanwhile, Hong Kong stocks gained nearly 15% in February, driven by optimism around DeepSeek, a Chinese AI company rivaling OpenAI, boosting Alibaba and Xiaomi shares. In Japan, inflation slowed to 2.2% in February but remained above the Bank of Japan’s target for the fourth straight month. Industrial production fell 1.1% in January but is expected to rise in February, signaling cautious optimism. Investors are closely watching U.S. inflation data, which could influence future interest rate decisions.

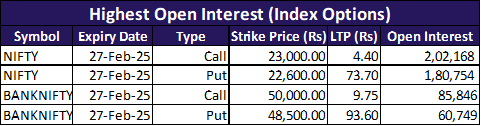

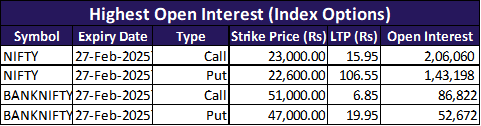

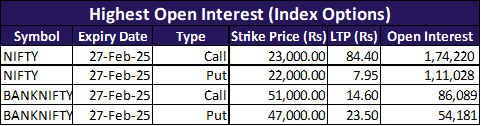

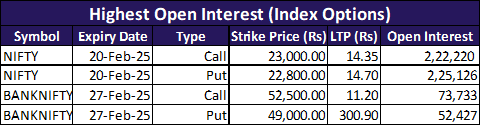

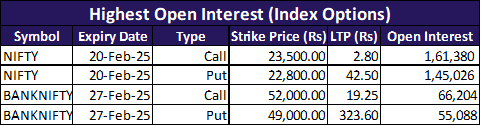

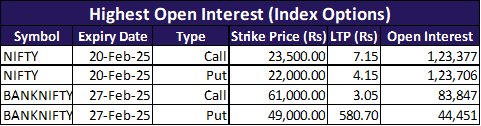

Option Traders Corner

Max Pain

Nifty 50 – 22600

Bank Nifty – 49500

Nifty 50 – 22555 (Pivot)

Support – 22,497, 22,450, 22,392

Resistance – 22,602, 22,660, 22,707

Bank Nifty – 48781 (Pivot)

Support – 48,589, 48,435, 48,244

Resistance – 48,935, 49,126, 49,280

Have you checked our latest YouTube Video

Did you know?

India’s Retail Investor Surge: Market Participation Hits Record Highs in 2024

India’s stock market has seen a 36% rise in retail participation, with over 50 million investors active by 2024. This surge is driven by increased financial literacy, digital trading platforms, and government initiatives. Systematic Investment Plans (SIPs) have also gained popularity, with monthly contributions hitting ₹14,000 crore in early 2025. These trends reflect growing confidence in India’s equity markets.