ITC Hotels: New Chapter

- 31st December 2024

Aaj Ka Bazaar

The early weakness on Wall Street reflected an extension of the sell-off seen last Friday, with some investors taking profits going into the end of the year. In US economic news, the National Association of Realtors reported that pending home sales surged much more than expected in November. Asian markets followed Wall Street lower this morning, though mainland Chinese and Hong Kong stocks bucked the weak trend to post marginal gains after the release of mixed PMI data. India’s benchmark indexes are set for a muted start on Tuesday, the final session of 2024, tracking other Asian peers, as elevated US Treasury yields continue to weigh on emerging markets. On stock-specific news, ITC Hotels, as a new entity post demerger, will have a firm zero debt balance sheet with cash and cash equivalents of Rs.1,500 crore to cater to robust growth going forward.

Markets Around Us

BSE Sensex –77,826.57 (-0.54%)

Nifty 50 – 23,550.60 (-0.40%)

Bank Nifty – 50,817.85 (-0.26%)

Dow Jones – 42,551.88 (-0.04%)

Nasdaq – 19,483.59 (-1.21%)

FTSE – 8,121.01 (-0.35%)

Nikkei 225 – 39,894.54 (0.00%)

Hang Seng – 20,111.18 (0.38%)

Sector: Hotels

ITC Hotels Gains ₹1,500 Crore Boost

ITC will transfer ₹1,500 crore in cash and assets, including trademarks, to its demerged hotel business, ITC Hotels, to support growth and contingency needs. Starting January 1, 2025, ITC Hotels will operate with a strong, debt-free balance sheet, generating cash to fund capital investments like renovations, ongoing projects, and new greenfield developments. The company plans to explore selective acquisitions and value-driven partnerships. Employees from ITC’s hotel division will transition to ITC Hotels with their current terms maintained. Shareholders of ITC will receive 60% of ITC Hotels’ equity, while ITC will retain the remaining 40%. Investments in non-hospitality ventures like EIH and HLV will remain with ITC. ITC Hotels will also manage operations at ITC Grand Central, Mumbai, under a service agreement. The demerger positions ITC Hotels for accelerated growth in the hospitality sector. Shares will be allotted to ITC shareholders based on January 6, 2025, as the record date.

Why it Matters:

The demerger enables ITC Hotels to operate independently with a strong, debt-free financial position, focusing on growth and strategic acquisitions. Shareholders benefit directly by owning equity in the hotel business, unlocking potential value. This move positions ITC Hotels to expand and compete effectively in the growing hospitality sector.

NIFTY 50 GAINERS

BEL – 289.55 (1.63%)

KOTAKBANK – 1765.15 (1.40%)

ONGC – 235.50 (1.23%)

NIFTY 50 LOSERS

TECHM – 1702.60 (-2.20%)

INFY – 1868.35 (-1.98%)

TCS – 4078.75 (-1.92%)

Sector: Ship Building

Mazagon Docks secures Rs 1.990-Crore Contract

Mazagon Dock has secured a Rs 1,990 crore contract from the Defence Ministry to build and integrate an Air Independent Propulsion (AIP) Plug for submarines, enhancing their underwater endurance. This technology, developed by DRDO with industry partners L&T and Thermax, allows diesel-electric submarines to operate longer without surfacing for oxygen. The AIP will be retrofitted onto Scorpene submarines, with the first expected during a refit in 2025. The project supports the ‘Aatmanirbhar Bharat’ initiative and is expected to create nearly three lakh man-days of employment. Additionally, the government signed an Rs 877 crore contract with Naval Group of France to equip Kalvari-Class submarines with Electronic Heavy Weight Torpedoes, boosting their firepower capabilities.

Why it Matters:

This project boosts India’s naval capabilities by extending submarine endurance with advanced Air Independent Propulsion (AIP) technology. It aligns with the ‘Aatmanirbhar Bharat’ initiative, reducing reliance on foreign systems. Additionally, it strengthens the defense sector and creates significant employment opportunities.

Around the World

Asian stocks remained quiet on Tuesday, following Wall Street’s drop amid low year-end trading volumes. Several markets, including Japan, South Korea, and Thailand, were closed, while others like Hong Kong and Australia operated shorter sessions. Chinese manufacturing data showed growth for a third month in December, supported by recent stimulus measures, but the slower-than-expected expansion raised concerns about the economy’s health amid a property crisis. Chinese markets fell slightly, while Hong Kong gained 0.7%. Investors await details on Beijing’s upcoming fiscal measures. Australia’s ASX 200 dropped 0.9%, reflecting concerns about China’s economic outlook. India’s Nifty 50 Futures dipped 0.2%, and Malaysia’s KLCI edged lower. Meanwhile, South Korea faces political turmoil, with President Yoon Suk Yeol arrested after his impeachment over imposing martial law. Markets in South Korea remained closed.

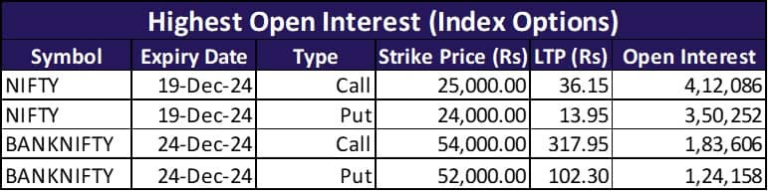

Option Traders Corner

Max Pain

Nifty 50 – 23,800

Bank Nifty – 52,000

Nifty 50 – 23,719 (Pivot)

Support – 23,524, 23,403, 23,208

Resistance – 23,840, 24,035, 24,156

Bank Nifty – 51,216 (Pivot)

Support – 50,454, 49,955, 49,192

Resistance – 51,715, 52,478, 52,976

Did you know?

Indian Digital Milestone Achieved

India has generated over 138 crore Aadhaar numbers, transforming digital identity verification. DigiLocker now serves 37 crore users, securely storing 776 crore documents. The DIKSHA platform has facilitated 556 crore learning sessions and achieved nearly 18 crore course enrollments.

Have you checked our latest Brand Ad ? Click Below to check now!